The date for authorisation for the so-called Pan-European personal pension product (PEPP) is fast approaching – 22 March 2022 – and yet the European pensions market seems to be relatively quiet about it.

Labelled as a cost-efficient pensions product tailored to consumer needs and portable EU-wide by EIOPA, a PEPP is a voluntary pensions product, complementary to state-based and occupational pensions.

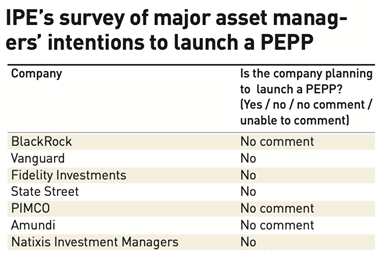

Those are all great reasons for a financial provider – insurer, occupational pension fund, asset manager, bank – to launch such a product and, as announced at PensionsEurope’s annual conference last summer by EIOPA’s executive director Fausto Parente, the authority is expecting 13 pan-European PEPP providers to launch products on the first day they are able to.

Yet there seems to be some hesitation, mainly to do with EIOPA’s proposed 1% fee cap on a basic PEPP product, which should include the initial cost of advice to members.

The PEPP has the potential to play an important role in delivering retirement savings to millions of European savers and the investment management industry is keen to manufacture such a product.

But there is a real risk that the decision to include the initial advice cost under the fee cap will prevent potential providers from developing an economically viable business model for the PEPP, and this could jeopardise its take-up.

The 1% fee cap is intended to include all costs for administration, asset management and distribution, as well as providing full cost transparency. Any costs linked to additional features that are not required cannot be included in the cap.

The cap is necessary to help make the PEPP attractive alongside guaranteed products, particularly in the current interest rate environment. Admittedly, capping the cost could affect the quality of service that a provider can afford to offer.

The purpose of the basic PEPP is to be a low-cost default investment option that would be assigned to the PEPP saver in absence of an active choice. Considering the high costs of investment products in the EU and the detrimental effects these have had on the returns, a cost cap of 1% for a basic PEPP is of absolute importance.

Venilia Amorim, Editor, IPE.com

venilia.amorim@ipe.com