Asset swap (ASW) spreads are currently trading at historically high levels as volatility in rates markets has remained high. We believe there is an opportunity for continental European pension funds to enter into Euribor receiver swaps and sell Bunds in their matching portfolio.

Indeed, we expect that the peak in ASW spreads has been reached and that swaps will outperform Bunds during the course of this year.

Rates markets seems to be in full risk-off mode

Since the beginning of this year, US Treasury and Bund yields rose sharply as central banks adopted the path of monetary policy normalisation, which is also reflected in the number of rate hike expectations priced in by financial markets.

Furthermore, rate hike expectations for the coming years, which are priced in by markets are an important driver of longer-term yields. Indeed, the 10-year Bund yield has a very high correlation with short-term rate expectations a few years ahead as shown in figure 1.

These yields have shown an unusual divergence since the beginning of this year.

Figure 1: Shortage of collateral and safe haven demand drives a wedge between euro rates

We believe this is driven by a shortage of collateral in combination with safe haven demand by investors. Both drive a wedge between short-term rate expectations a few years ahead and the 10-year Bund yield.

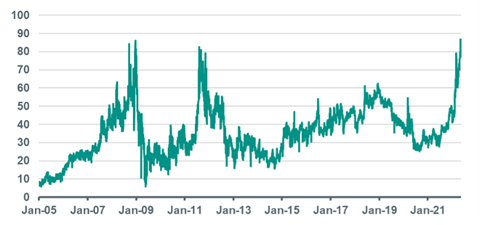

Looking at ASW spreads, the difference between Bund yields and swap yields, gives us the same picture. Indeed, ASW spreads are trading at elevated levels and just below the levels which we have seen during the global financial crisis and the European sovereign debt crisis as shown in figure 2.

Figure 2: Swap spreads are trading just below the levels of the great financial crisis and European sovereign debt crisis

Normally, the 2-year, 5-year and 10-year ASW spreads follow measures of bank risk quite closely as banks are the main counterparties in these transactions, whereas the 30-year ASW spread follows the relative credit worthiness of banks over Germany.

However, the credit default swap (CDS) of banks – which we use as a proxy for the credit worthiness of banks – has come down after a spike following the Russia/Ukraine conflict.

Nevertheless, ASW spreads are still trading at elevated levels, which in our view is partly driven by the relatively high volatility in rates markets as shown in figure 3.

Figure 3: Swap spreads increased significantly on the back of volatility in rates markets

In our assessment, the relative high volatility in rates markets since February has been driven by the Russian invasion of Ukraine in combination with market expectations of central bank policy rates, which have varied from day to day.

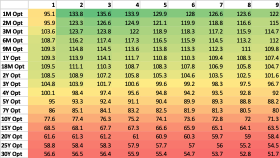

Indeed, uncertainty around the path of central bank policy rates seems to be an important driver as volatility has been especially high in the short-end of the curve as shown in the volatility matrix below. Also our inflation option model, in which we estimate a probability density distribution for inflation based on inflation swaptions with a 2-year expiry, shows that the uncertainty around inflation in the euro area is still relatively high.

As European Central Bank (ECB) policy is based on the outlook for inflation, this implies that uncertainty around ECB policy rates is also high. Consequently, it makes sense that volatility in rates markets is especially high in the short-end of the curve (figure 4).

Figure 4: Volatility in rates markets highest in the short-end of the curve

Looking further ahead we expect swap spreads to tighten again, but to settle at elevated levels

We expect volatility in rates markets to settle down once financial markets gauge the impact of monetary policy tightening. Uncertainty around the path of central bank policy normalisation will decline during the course of this year once the inflation outlook and central bank reactions to a deteriorating growth-inflation mix becomes clearer.

On the back of this we expect volatility in rate markets to come down and therefore ASW spreads to tighten.

Besides this, we also expect that technicals will be favourable for tighter ASW spreads, as the relative demand for sovereign bonds will decrease versus swaps, as net asset purchases by the ECB are expected to end altogether in Q3.

Finally, we expect that solid bank fundamentals, a key driver of ASW spreads, will also be supportive for ASW spreads.

Capital positions of banks have risen substantially over the past few years, now being at historically high levels. In addition, the outlook for provisions remains very manageable for European banks, which is a strong support metric for the credit worthiness of banks.

Meanwhile, rising rates will also reduce pressure on net interest income of banks. As such, bank fundamentals will remain solid throughout the year, which should increasingly come to the fore. This should exert downward pressure on ASW spreads.

Pension funds are able to take advantage of elevated ASW spreads in their matching portfolio

Continental European pension funds have significant amounts invested in sovereign bonds, especially Bunds, in their matching portfolios. As we expect swaps to outperform Bunds during the course of this year, it is an attractive entry point to enter into Euribor receiver swaps and sell Bunds.

We expect that 2-year, 5-year and 10-year ASW spreads will outperform the 30-year ASW spread, as the latter is relatively more stable.

In addition, the 2-year area seems to be most attractive from a carry- and roll down perspective. Indeed, the carry- and roll down of receiving 2-year Euribor swap and selling the DBR February 2024 is almost 20bps based on a 6-month investment horizon.