Accounting for Scope 3 is challenging, but integrating these emissions allows for better monitoring of pathways to decarbonisation

Scope 3 emissions, which break down into suppliers’ emissions and emissions from the and disposal of the company’s products, have proven much more difficult for companies to account for than Scopes 1 or 2, both of which are under their direct control.

The lack of standardised methodology and the need to rely on modelling have until now led to a limited and cautious integration of Scope 3 data into investment processes. The intrinsic complexity has hindered integration so far.

European regulation acknowledges these difficulties: the climate benchmark regulation allows for a four-year transition period for the inclusion of Scope 3 data and companies have until January 2023 to include them in their reporting under the EU sustainable finance disclosure regulation.

However, there are strong limitations to Scope 3 data reliability, such as breadth and accuracy of company reporting, comparability, and double counting issues for “portfolio footprinting”.

Even if the number of public companies reporting Scope 3 emissions in 2021 grew 30% from 2020, more than 40% of companies reporting Scopes 1 and 2 are still not reporting Scope 3 – a trend that has remained unchanged for the last three years[1].

Assessing Scope 3 emissions for reporting requires internal modelling capacities or additional reliance on third party expertise. When companies do report, they often omit part of their Scope 3 emissions and, according to our analysis, only 30% of companies rely on external verification processes to increase accuracy and completeness.

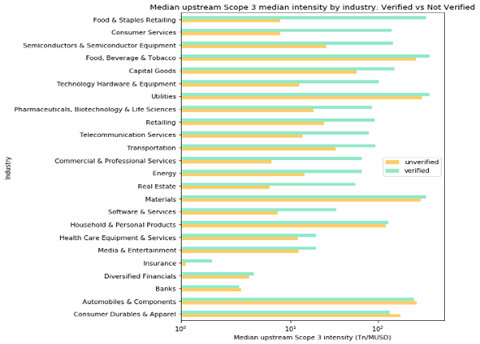

We found that there is a 44% difference between the medians of Scope 3 emissions for verified and unverified reports. As shown in the chart below, the effect persists when conducting the analysis at industry level[2].

Per industry comparison of median verified and not verified Scope 3 upstream intensities

Even with the existing GHG protocol framework[3], reported Scope 3 emissions strongly vary with regards to the modelling assumptions and the inventory boundary, which makes it difficult to compare.

Third party models have work to do to overcome this issue but divergences among data providers remain very high[4].

Lastly, integrating Scope 3 at the portfolio level will lead to double accounting which is complex to adjust for beyond an approximated discount rate.

As the shift towards low carbon development pathways becomes an even stronger imperative, Scope 3 emissions can no longer be ignored. The recently published SBTi Corporate Net Zero Standard requires companies with Scope 3 emissions that are at least 40% of total emissions to set near-term science-based Scope 3 targets.

According to our research, that could apply to over 87% of companies[5]. SBTi will update this year its Scope 3 target setting methods and criteria to ensure full alignment with its Net Zero Standard[6].

From a macroeconomic point of view, the integration of Scope 3 also allows for better monitoring of pathways to decarbonisation. The net carbon content of national trade balances represents a country’s Scope 3 emissions. Imported goods will be consumed locally but have generated GHG emissions in other countries for their production. Exported goods have generated emissions locally but will be consumed in other countries.

For example, while emissions per capita in France for Scopes 1 and 2 (i.e. produced emissions) are 50% lower than in Germany, the two countries are comparable when accounting for Scope 3 (i.e. consumed emissions)[7]. This is closely related with financial materiality of climate impact[9], as implementation of a carbon border tax is high on the political agenda in Europe and will impact the competitiveness of exporters when matched to the carbon intensity of their value chain.

To overcome these limitations, corporations and countries need a way to deliver consistent Scope 3 data and to integrate upstream and downstream emissions into their reporting.

Investors too must rely on data to ensure their sustainable analysis of portfolio holdings is robust. Latest news on SEC upcoming climate disclosure requirements for SEC filings mentioned potential mandatory Scope 3 disclosure.

Quantity and quality of reported Scope 3 emissions by corporates will likely increase driven by different factors, for example more stringent regulatory requirements like the EU Corporate Sustainability Reporting Directive and TCFD, and deployment of cloud-based climate performance reporting and management tools.

But regulation can only take us so far. Technology which offers a robust and consistent methodology to deliver Scope 3 emissions at scale with deep granularity and full transparency will allow investors to better manage their paths to decarbonisation, while also expanding their engagement strategy to supply chain emissions. The need will remain for coverage expansion – for example to private markets – and reliability, including consistency assurance and clear comparability.

Patricia Pina is head of research & innovation at Clarity AI, a sustainability analytics platform

——

[1] Clarity AI research based on CDP data

[2] Clarity AI research based on CDP data

[3] https://ghgprotocol.org/standards/scope-3-standard

[4] A comparison of Scope 3 data from two providers that we conducted for 600 European companies showed that they diverged on average by 112%

[5] Clarity AI research based on CDP data

[6] SBTi Climate Action in 2022

[7] Between 11 and 12 to of CO2eq per capita, France has a structural trade deficit linked to energy import whereas Germany has a structural trade surplus leading to a neutral carbon content of its trade balance.

[8] Which now needs to be assessed under a growing number of regulations including SFDR, climate stress-testing for banks and insurances and TCFD.