The European Securities and Markets Authority (ESMA) has today published a briefing to promote a common approach across the EU to supervising fund managers’ sustainability-related disclosures and integration of sustainability risks.

It said a common approach should serve to increase transparency for investors and avoid the practice of “greenwashing”.

The background to the supervisory briefing includes new requirements applicable to asset managers, such as under the sustainable finance disclosure regulation (SFDR) and the taxonomy regulation. It comes after the US Securities and Exchange Commission last week proposed new ESG names rules and strategy disclosure rules.

Writing on LinkedIn, Antoine Bargas, head of regulatory at BNP Paribas Securities Services, referred to ESMA’s briefing, which is non-binding, as a “to-do list” for national competent authorities on how to best deal with greenwashing in asset management.

It covers two main areas:

- guidance for the supervision of fund documentation and marketing material, as well as guiding principles on the use of sustainability-related terms in funds’ names; and

- guidance for convergent supervision of the integration of sustainability risks by AIFMs and UCITS managers.

Points made with respect to the former include that the recital of the SFDR delegated regulation warns against greenwashing risks where funds apply “non-binding” exclusion strategies, and that sustainability-related disclosures should not use technical jargon that may not be understood by the average investor.

ESMA also said that “without giving the impression of a ‘label’ to investors”, an indication as to under which article of the SFDR (and if relevant, the taxonomy regulation), the fund manager discloses the relevant information should be mentioned in the fund documentation.

Fund names

On fund names, ESMA suggested supervisors could be justified to reject reference to a specific theme or pillar in a fund name if it does not demonstrate relevant binding sustainability characteristics.

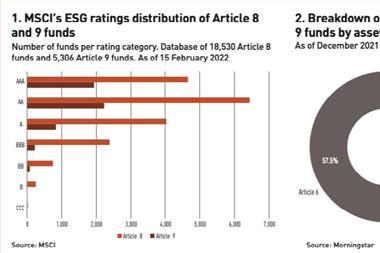

It also said it was advisable that the terms “sustainable” or “sustainability” should be used only by funds disclosing under Article 9 of the SFDR; funds disclosing under Article 8 of the SFDR which in part invest in economic activities that contribute to environmental or social objectives, and funds disclosing under Article 5 of the taxonomy regulation.

It also said the words “impact” or “impact investing” or any other impact-related term should be used only by funds whose investments are made with the intention to generate positive, measurable social and environmental impact alongside a financial return.

ESMA’s briefing also includes some examples of acceptable and non-acceptable fund names.

With respect to the supervision of the integration of sustainability risks by fund managers, ESMA noted that this integration is required from 1 August 2022 and that supervisory controls should review the implementation and application of policies and procedures relating to aspects such as investment due diligence, risk management, and recruitment and human resources.

Publication of the supervisory briefing comes shortly after the European Commission published its response to the European Supervisory Authorities’ questions about how to interpret certain SFDR provisions, with sustainble investment trade body Eurosif saying the Commission had provided much-needed clarity around product-level disclosures.

For example, Eurosif said that financial market participants are now permitted to use estimates and ‘complementary assessments’ on the level of taxonomy-alignment of investee companies in cases where the latter are not required to disclose their level of taxonomy-alignment and for which “complete, reliable and timely information could not be obtained”.

However, the use of estimates should be clearly explained and justified to end investors.

To read the digital edition of IPE’s latest magazine click here