The new EU-wide label for green bonds will improve transparency and as such will make it more difficult for companies to engage in greenwashing, according to investors. It may also revive the premium investors were once willing to pay for green bonds, the so-called greenium, which has recently all but evaporated.

Several weeks ago, European lawmakers struck a provisional deal on a new Green Bond Standard (GBS), which would require eligible green bond issues to be at least 85% aligned with the green taxonomy.

“The risk of ‘greenwashing’ will be drastically reduced with these decisions,” said Peter Jeggli, head of portfolio management at ESG-AM, in a recent paper.

Wilfried Bolt, senior investment manager for fixed income rates and mortgages at Dutch pension asset manager PGGM, also welcomed the new European label, which is supposed to come into force by 2024, “because the conditions bonds need to meet to get it will considerably help us in screening and rating loans available in the market.”

Spectacular growth

The green bond market has grown dramatically since 2007, to just under $500bn by 2022. The first green bonds were issued by European governments, later followed by corporates. Most green debt is still issued in Europe, but green bonds are also on the rise in the US and Asia. The big question now is whether the European GBS, the world’s first green bond label, will also be recognised internationally.

“It is great that we are now finally getting such a standard in Europe. But what I fear is that in the rest of the world they will soon develop their own standards,” noted Erwin Houbrechts, manager sustainable investments at Dutch pension fund PGB earlier this month, speaking at a breakfast meeting on investing in green bonds in Utrecht.

“At the moment, we don’t have any bonds in our portfolio that are fully aligned with the European GBS, and only a tiny portion of the overall market will be,” said Théo Kotula, an ESG analyst at AXA Investment Managers.

“If you want to claim you’re fully aligned with the taxonomy, you have to also comply with a range of minimal social safeguards related to things like human rights, supply chain management,” he added.

Definitions of these additional criteria are yet to be set, and Kotula expects issuers to thread cautiously. “They will not want to overclaim their alignment with the taxonomy to avoid being accused of greenwashing,” he said.

High bar

The vast majority of green bonds do not yet meet the GBS’s requirement that at least 85% of the proceeds must be spent on green projects, is the assessment of most investors. According to Kotula, it will be especially difficult for sovereign issuers to meet the GBS criteria.

“Maybe the taxonomy is inherently tilted to corporates, as it is more difficult for sovereigns to measure alignment,” he noted. This is because most governments tend to not issue debt for specific projects.

According to a recent investigation by Commerzbank, about half of euro green bonds issued by (supra)national governments do not meet the threshold of 85% of expenditure linked to the taxonomy.

But this need not to necessarily be a problem, added PGGM’s Bolt. “Bonds will not need to have a European GBS label to be regarded as a sustainable investment by us,” he said.

Greenium

The GBS label will have an immediate impact on the green bond market, though. Currently, investors make little distinction between different green bonds in terms of sustainability because of the lack of hard criteria bonds need to meet in order to be called green.

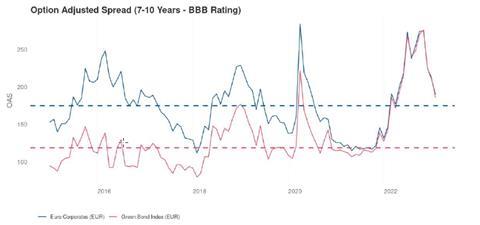

The so-called greenium, the difference in yield between ‘grey’ and green bonds, has fallen significantly (see graph).

“Our observations showed that the greenium for the A-rated EUR issues in the 7-10 year bucket has changed in sign over the last few years. Mean spread differences have hovered around 20 basis points and are currently pricing in a slightly negative greenium,” said Jeggli.

“From an issuer perspective, the days of large discounts when issuing green bonds are over,” he added.

The arrival of the GBS could revive the greenium, noted Kotula. “I think there will be a kind of race to be the first issuer that is GBS-aligned or certified. Having a GBS-label will certainly affect demand for an issue.”

On the other hand, the advent of the GBS can also impact the existing stock of green bonds, noted PGB’s Houbrechts. “If you turn out to invest in bonds that you considered to be green but they turn out not to meet the GBS criteria, you not only risk losing some money because your bond will be valued lowe; it’s also a reputational risk,” he said.

The latest digital edition of IPE’s magazine is now available