The global share of actively managed assets fell below 70% last year as market-benchmarked passive and indexed strategies have continued to gain ground. This is according to IPE’s latest benchmark global asset management research study, IPE Top 500 Asset Managers, published today.

European institutional investors have also continued their shift to passive – which now accounts for fully 25% of client managed assets. Some 80% of client assets were actively managed until as recently as 2022 but last year saw the most pronounced shift away from active in recent years, IPE’s data shows.

IPE’s findings follow recent data confirming the global shift in client preferences. LSEG Lipper reported earlier this year that global passive equity fund net assets surpassed those of actively managed funds for the first time at the end of 2023 – counting $15.1trn for passive funds and $14.3trn for active.

However, IPE measures a much larger sample of data derived directly from an extensive survey of global asset managers and research exercise, conducted between February and May of this year. The data covers all client assets managed in funds and separately managed accounts – both globally and for European institutional business.

The findings underscore the revenue pressures of many asset management firms as ad valorem fee income has failed to keep pace with rising costs.

Continued cost pressures

Tony Gaughan, EMEA investment and wealth management sector lead at Deloitte, said: “The passive trend in both EMEA and North America continues to have material significance for active managers, compounding pressure to deliver performance, demonstrate added value and justify fees.

“At the same time, from a corporate perspective, this trend drives increasing margin pressure, consolidation to deliver benefits of scale, and makes critical the search to acquire or build other alpha delivering capabilities such as private assets.”

Dean Frankle, managing director and partner at Boston Consulting Group, pointed to clear global demand for passive strategies with passive net inflows of nearly $1trn in 2023 and active net outflows of around $800bn. He also noted the 15% reduction in average fund price points since 2010, to 22bps, compared with an 80% increase in costs over the same period.

Frankle said: “Historically, the industry has managed to absorb this cost pressure as market appreciation drove revenue growth; however, despite AUM more than doubling, revenue has only increased [around] 75% during the same period.

“In response, asset managers need to continually focus on ways to drive productivity, offer more personalised product offerings, and extend into private markets to help fend off revenue – leveraging AI to drive the next wave of transformation.”

Kamil Kaczmarski, asset management partner for Oliver Wyman, based in Frankfurt, noted the clear shift away from traditional core active strategies in favour of both low cost passive strategies on the one hand and private markets on the other.

He said: “This presents a considerable challenge for even large global diversified asset managers. For every billion of outflows on the active side, they must attract 3-4 billion in inflows on the passive side to maintain their revenue base. As a result, many active asset managers without a scalable passive offering are exploring more systematic approaches to develop low-cost, low tracking-error products.”

“We anticipate that this trend will continue to accelerate in the coming years, leading to the adoption of more systematic and quantitative techniques in the investment process. Artificial intelligence will undoubtedly play a significant role in catalysing this shift.”

Kaczmarski also pointed out that passive assets under management in Europe are growing at a rate three times faster than active assets.

Amin Rajan, chief executive officer of CREATE-Research, said that for some, the true test of passives “was best judged not when markets were […] artificially inflated, but by their resilience when central banks take away the proverbial punch bowl, causing markets to tank”.

He added: “This happened in 2022-23 but stock pickers have continued to struggle, despite having higher degrees of freedom.”

Rajan also pointed to the various responses of active managers – which include diversifying into ETFs, improving investment capabilities, adding private market capabilities and M&A.

“The actions so far have yet to arrest the relative decline of active funds. The majority of pension investors believe that the pendulum is unlikely to swing back any time soon.”

Net asset flows return to positive territory

IPE’s study also finds an anaemic return to relative health for asset managers globally in 2023. Last year’s net flow figure was 2.39% of measured AUM – a jump back into positive territory following net client outflows of -0.36% in calendar year 2022, but considerably less than the previous year’s health 4.02% figure.

European institutional net flows also rebounded, but to 2.77% last year, compared with -1.09% the year before. The sluggish return to net growth here is more pronounced as this client segment enjoyed net flows of well over 4% for the three preceding years.

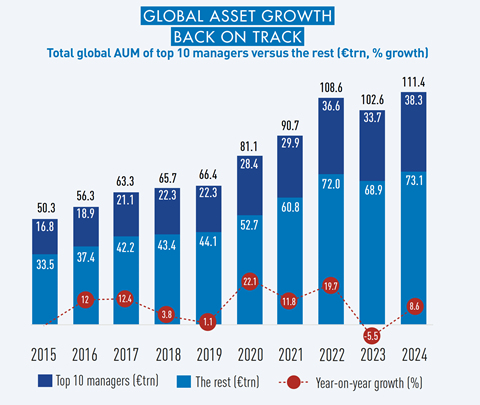

Overall AUM measured across the industry grew 8.6% in 2023, reaching €111.4trn ($120trn). Last year’s data saw a dip of 5.5% in global assets across calendar year 2022 as managers faced negative asset returns in both equities and bonds.

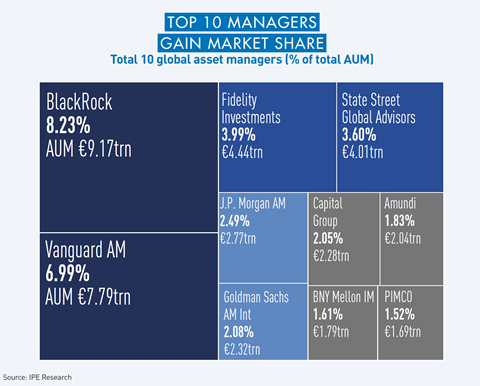

Amundi remains the only European house in the US-dominated top 10. UBS Asset Management is bumped up to eleventh place this year (the acquisition of Credit Suisse’s asset management business did not close in time to be reflected in last year’s figures).

BlackRock keeps its crown as the largest manager of European institutional assets and Amundi jumps from sixth position to fourth, reflecting a 20% rise in client AUM for this business segment.

The 2024 Top 500 Asset Managers report and downloadable dataset is now accessible with an IPE Professional Membership package, click here to learn more.

Data in this article has been amended following initial publication to correct a calculation error