Sponsored commentary from Lombard Odier Investment Managers

In this investment viewpoint we describe seven key misconceptions that we think may have deterred investors from fully integrating considerations linked to scope 3 emissions and lead to confusion in the market.

Scope 3: Indirect emissions linked to supply chains and product use

In the same way that companies’ financial reports are subject to strict accounting rules and procedures, so too are companies’ greenhouse gas (GHG) emissions. However, there is only one global standard for GHG emissions reporting (The Greenhouse Gas Protocol)1. Accounting for one’s carbon emissions requires specific expertise and understanding of this Protocol. In particular, understanding and appreciating the nuances of different parts of a company product’s lifecycle (known as scope 1,2 and 3 emissions) is critical.

Misconception 1: Scope 1 and 2 emissions are comprehensive enough

Many investors still focus primarily on scope 1 and 2 emissions, believing that this provides a reasonable insight into most companies’ carbon footprints. However, for key industries (e.g. oil, gas and automotive sectors) and all major sectors, excluding utilities, scope 3 are the dominant type of emissions. Therefore, if investors do not take scope 3 emissions into account, they fail to capture a company’s full GHG profile.

Misconception 2: Scope 1 and 2 emissions are more important due to corporate control

This view can be challenged on three accounts:

- First, companies have significant influence over their supply chains and can engage suppliers to reduce emissions.

- Second, companies can directly reduce their supply-chain emissions by transitioning to less carbon-intensive business models.

- Third, even where a company’s ability to influence scope 3 emissions may be limited, the company’s exposure to these emissions still creates significant transitional risks – driven by regulatory and market forces.

Misconception 3: There is insufficient data to meaningfully assess scope 3 emissions

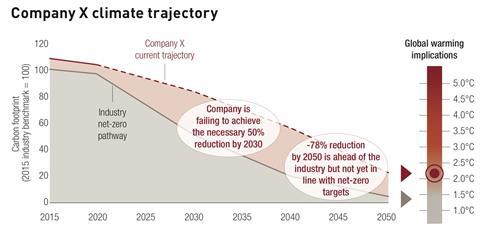

In 2010, less than 3,000 companies disclosed information to the Carbon Disclosure Project, but as of 2020 this had grown to over 9,500. While a smaller number of these disclose scope 3 data, this proportion has also grown. Furthermore, what is often overlooked is that scope 3 emissions can often be assessed even if they are not reported. Using the automotive sector as a case study, our report finds that such models can be more accurate than company-reported figures.

Misconception 4: Emissions double-counting occurs within portfolios

If an investor holds an oil and gas and a transport company in the same portfolio, would the oil and gas company not be reporting emissions that are also already counted by the transport company? We believe not - these issues are often misrepresented in overly stylised examples that fail to recognise that it would be unusual for more than a small share of a company’s suppliers to feature in the same portfolio. Double-counting of emissions should be considered from an economy-wide, rather than portfolio, perspective.

Misconception 5: Double-counting is undesirable and should be adjusted for

While addressing misconception #4, we recognise that a significant amount of double counting does occur. But, the question frequently forgotten is: whether such double counting is in fact undesirable? We argue that although emissions are double-counted across a value chain, carbon risks also reverberate through supply chains. While double-counting may recognise that companies share responsibility for emissions, it artificially deflates the true scale of a portfolio’s carbon exposure and the financial risks that it entails.

Misconception 6: As data are still improving, it makes sense to defer scope 3 analysis

Given the misunderstandings about scope 3 analysis, some investors are taking a cautious approach. At best, they are investigating indirect emissions in a handful of sectors only. We believe that delaying scope 3 analysis across the economy will result in significant turnover in investors’ portfolios. In the process, this could lead to investors selling hidden, poorly aligned companies only after they have already depreciated due to scope 3 emissions disclosure, and equally drive appreciation among better-aligned companies before investors lagging on scope 3 analysis have identified them.

Misconception 7: High scope 3 emissions disqualify companies from a climate-aligned portfolio

Including scope 3 emissions in investment analysis improves the accuracy of carbon-risk assessments in portfolios, but does not mean that high-emitting companies should necessarily be excluded. Carbon-intensive industrial sectors are often not only essential to the economy, but are also among the most important in the net-zero transition.

The right question is therefore not whether a company is emissions intensive today, but whether it is transitioning quickly enough to meet Paris Agreement-aligned decarbonisation objectives.

FOOTNOTES

1 We set the standards to measure and manage emissions / https://ghgprotocol.org/

This forward-looking assessment requires genuine carbon expertise, including new assessment capabilities such as implied temperature rise (ITR) metrics, which Lombard Odier already offers.

IMPORTANT INFORMATION: For professional investor use only. This document has been issued by Lombard Odier Funds (Europe) S.A. a Luxembourg based public limited company (SA), having its registered office at 291, route d’Arlon, 1150 Luxembourg, authorised and regulated by the CSSF as a Management Company within the meaning of EU Directive 2009/65/EC, as amended; and within the meaning of the EU Directive 2011/61/EU on Alternative Investment Fund Managers (AIFMD). The purpose of the Management Company is the creation, promotion, administration, management and the marketing of Luxembourg and foreign UCITS, alternative investment funds (“AIFs”) and other regulated funds, collective investment vehicles or other in- vestment vehicles, as well as the offering of portfolio management and investment advisory services. Lombard Odier Investment Managers (“LOIM”) is a trade name. This document is provided for information purposes only and does not constitute an offer or a recommendation to purchase or sell any security or service. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful. This material does not contain personalized recommendations or advice and is not intended to substitute any professional advice on investment in financial products. Before entering into any transaction, an investor should consider carefully the suitability of a transaction to his/her particular circumstances and, where necessary, obtain independent professional advice in respect of risks, as well as any legal, regulatory, credit, tax, and accounting consequences. This document is the property of LOIM and is addressed to its recipient exclusively for their personal use. It may not be reproduced (in whole or in part), transmitted, modified, or used for any other purpose without the prior written permission of LOIM. This material contains the opinions of LOIM, as at the date of issue. Neither this document nor any copy thereof may be sent, taken into, or distributed in the United States of America, any of its territories or possessions or areas subject to its jurisdiction, or to or for the benefit of a United States Person. For this purpose, the term “United States Person” shall mean any citizen, national or resident of the United States of America, partnership organized or existing in any state, territory or possession of the United States of America, a corporation organized under the laws of the United States or of any state, territory or possession thereof, or any estate or trust that is subject to United States Federal income tax regardless of the source of its income. Source of the figures: Unless otherwise stated, figures are prepared by LOIM. Although certain information has been obtained from public sources believed to be reliable, without independent verification, we cannot guarantee its accuracy or the completeness of all information available from public sources. Views and opinions expressed are for informational purposes only and do not constitute a recommendation by LOIM to buy, sell or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change. They should not be con- strued as investment advice. No part of this material may be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorised agent of the recipient, without Lombard Odier Funds (Europe) S.A prior consent. In Luxembourg, this material is a marketing material and has been approved by Lombard Odier Funds (Europe) S.A. which is authorized and regulated by the CSSF. ©2021 Lombard Odier IM. All rights reserved.