Leading sustainability reporting organisations have come together to agree a shared vision of what is needed to help resolve confusion surrounding sustainability disclosure and develop what they describe as a more coherent, comprehensive corporate reporting system.

The organisations said they were also publishing a joint statement of intent to drive towards this goal, by working together and by each committing to engage with key actors, including IOSCO and the IFRS, the European Commission, and the World Economic Forum’s International Business Council.

Mardi McBrien, managing director at the Climate Disclosure Standards Board (CDSB), said the joint statement was “a natural next step as we look to form a complete picture of how these standards might complement financial GAAP – integrating with the TCFD”.

“We are looking forward to developing this picture further in the near future to meet the growing demands of investors, governments and consumers globally.”

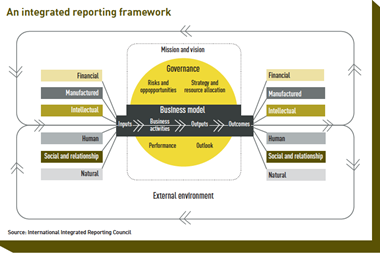

Between them, the organisations guide the majority of sustainability reporting. GRI, SASB, CDP and CDSB set frameworks and standards for sustainability disclosure, while the International Integrated Reporting Council (IIRC) provides a framework that connects sustainability disclosure to reporting on financial “and other capitals”.

‘The time is now’

For a long time there have been concerns about the corporate sustainability disclosure area being an “alphabet soup”. The five organisations said sustainability disclosure was “necessarily more complex than financial reporting” and that this complexity had made it difficult to develop a comprehensive solution for corporate reporting, which was urgently needed.

However, conditions were “ideal for rapid progress,” they said.

There was growing appetite from regulators, policymakers and others to respond to a “groundswell of demand to understand the connection between sustainability topics and financial risk and opportunity, along with the contribution of business to achieving the Sustainable Development Goals”.

In the EU, for example, the European Commission has kicked off a process to develop possible EU non-financial reporting standards, with the members of a task force working on this announced last week. It is also due to review legislation on non-financial reporting by corporates.

“We believe that the conditions are ripe for the development of a market-based and globally coherent solution for sustainability disclosure standards”

The independent sustainability reporting standard-setters, meanwhile, together with the IIRC, were increasingly collaborating, they said, with their efforts representing “natural building blocks for progress towards a comprehensive corporate reporting system”.

“The time is now,” the organisations said. “We believe that the conditions are ripe for the development of a market-based and globally coherent solution for sustainability disclosure standards.”

They called for support and engagement from sustainability disclosure users, including by providing feedback on the ideas expressed in their paper and by recognising that their frameworks and standards “naturally form part of a coherent eco-system, and can be used in a complementary way, especially in view of our description of dynamic materiality”.

According to the organisations’ paper, their joint statement of intent also serves as a “summary of alignment discussions” and was facilitated by the Impact Management Project, World Economic Forum and Deloitte.

The collaboration between the five organisations comes on top of bilateral efforts and ongoing work by the individual groups to maintain their standards.

The GRI, for example, has been consulting on revisions to its universal standards, with the manager of Norway’s sovereign wealth fund calling for these to include indicators about actual outcomes of work companies do to improve human rights.

Looking for IPE’s latest magazine? Read the digital edition here.

Topics

- Carbon Disclosure Project (CDP)

- ESG

- European Financial Reporting Advisory Group (EFRAG)

- GAAP

- Global Reporting Initiative (GRI)

- International Financial Reporting Standards (IFRS)

- International Integrated Reporting Council (IIRC)

- IOSCO

- non-financial reporting

- Non-Financial Reporting Directive (NFRD)

- Sustainability

- Sustainability Accounting Standards Board (SASB)

- sustainable finance