The 11 UK local government pension schemes (LGPS) forming the ACCESS asset pool have launched a tender for a regulated operator to set up and run a collective investment scheme.

The operator will be responsible for establishing and operating an Authorised Contractual Scheme and other collective investment vehicles exclusively for the asset pool.

The ACCESS asset pool expects to have around 25 to 35 sub-funds. The operator should make sure all major asset classes to be available, including as a minimum, equities, fixed income, multi-asset and property.

The tender is being managed by Kent County Council, one of the 11 ACCESS pool-administering authorities. The others are the councils for Cambridgeshire, East Sussex, Essex, Hampshire, Hertfordshire, Isle of Wight, Norfolk, Northamptonshire, Suffolk, and West Sussex.

The ACCESS pool is expected have around £33.9bn (€33.7bn) in assets once fully operational.

The pool’s plan for a third-party manager contrasts with the structure of other LGPS pools such as Brunel and London CIV, which have both chosen to build internal teams and capabilities.

Transition management provider panel for LGPS

Several LGPS funds have come together to establish a framework agreement for transition management services.

Norfolk County Council last week launched a tender as the council with lead responsibility for the LGPS’ tendering framework. The participating LGPS – representatives of six of the UK’s eight emerging asset pools – are looking for providers of transition management and implementation services, transition execution services, and transition management advisory services.

Bedford Borough Council, Carmarthenshire, Derbyshire and Suffolk County Councils, Brunel Pension Partnership and the London CIV are working together on the tender, but the framework can be used by other public sector pension bodies.

The eight asset pools must be ready for assets to be moved from individual LGPS funds by April next year, according to the government’s plans.

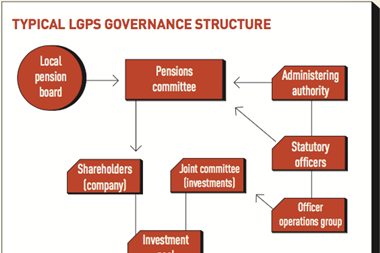

Pension fund governance: major gaps

Many small and medium-sized UK pension schemes are falling far short of meeting the governance standards expected by the Pensions Regulator (TPR).

Publishing findings from surveys of how defined benefit (DB) and defined contribution (DC) schemes are meeting TPR’s expectations, the regulator said the surveys were disappointing for individual small and medium schemes, highlighting major gaps in standards.

For example, many small and medium DC schemes were not meeting standards for investments as they failed to set appropriate investment strategies for their default funds.

Anthony Raymond, acting executive director for regulatory policy at TPR, said: “As part of our commitment to be a clearer, quicker and tougher regulator, we will be stepping up our regulatory action in cases where trustee boards fail to meet minimum legal standards, and we will publish the details of that action.

“We will also continue to examine whether sub-standard schemes should be consolidated with larger, well-run schemes.”

The regulator released its survey findings and response to them a day after the pension scheme trade body urged TPR to change its approach to pension fund governance.