The sustainable finance disclosure regulation represents a steep learning curve for most firms, says Emma Bickerstaffe, ESG & sustainability director at asset management consultancy MJ Hudson

As the number of funds touting positive environmental, social and governance (ESG) credentials increases, it is becoming increasingly difficult for individuals to distinguish fact from fiction and determine which funds are truly invested responsibly and which funds are merely ‘greenwashing’. The EU set out to address this challenge by introducing the Sustainable Finance Action Plan in March 2018.

Two of the key legislations in the European Commission’s plan are the sustainable finance disclosure regulation (SFDR), which introduces new sustainability-related disclosure obligations for financial market participants (FMPs) marketing their products in the EU, and the EU taxonomy regulation, which is essentially a dictionary for describing what constitutes environmentally sustainable activities.

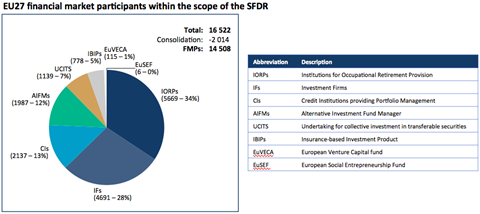

Over 14,500 FMPs fall within the scope of SFDR, including pension funds. Under SFDR, these FMPs are required to disclose qualitative and quantitative information on their approach to ESG, including the management of sustainability risks – that may impact the value of their investments – and principal adverse impacts – the potential negative impacts that their investments have on the environment and society.

The taxonomy regulation is a foundational building block in the EU’s action plan and forms part of several other regulations, including the SFDR and the Non-Financial Reporting Directive (NFRD). Some member states have declared that pension funds are classified as public interest entities and are therefore required to report under the NFRD.

A continuing source of ambiguity is that the Taxonomy has some conflicting timelines. FMPs offering Article 8 or 9 products with environmental characteristics are required to report on taxonomy alignment from 1 January 2022, while companies falling under scope of the NFRD are only required to do so from 1 January 2023 onwards.

Another is that the Taxonomy is incomplete. Only the criteria for two of the six environmental objectives have been published, with the remainder to follow in the first half of 2022.

Although the intentions behind these regulations are widely supported, the approach taken to implement them has been less well received. Incomplete and complex reporting requirements, phased execution and moving deadlines have caused confusion and resulted in uncertainty, and in some cases inactivity, across the industry.

The documentation firms are required to produce under the SFDR are grouped into entity-level and product-level disclosures. Entity-level disclosures apply to all FMPs that fall within the scope of the SFDR and came into force on 10 March 2021. A number of product-level disclosures also came into force then.

All products marketed after that date should have already supplemented their pre-contractual documentation (prospectus/PPM) with information relating to how sustainability risks are integrated into investment decisions including an assessment of the likely impacts of those risks on the returns of the products.

Products that promote environmental or social characteristics (also known as Article 8 or ‘light-green’ products) or that have a sustainable investment objective (Article 9, ‘dark-green’) are required to disclose additional information in their pre-contractual documentation, periodic reporting (annual report) and the website, explaining why it has been labelled as such and how its objectives are measured.

On 25 November 2021, the European Commission (EC) announced that it would delay the active date of level 2 of the SFDR, otherwise known as the Regulatory Technical Standards (RTS), to 1 January 2023 (following an earlier delay from 1 January 2022 to 1 July 2022).

The RTS are an important addition to the regulation as they specify the way certain SFDR disclosures should be presented, aiming to increase the quality and comparability for end-investors. Most importantly, the RTS provide templates for the Article 8 and 9 product-level disclosures and the statement on the consideration of Principal Adverse Impacts (PAI) at entity level.

For product level disclosures, institutional pension funds are reliant on the reporting and assessment of assets conducted by their asset managers who they allocate to. Many institutional investors are starting to build these new reporting commitments into their agreements to ensure they receive the information they need.

Although not legally required, we would also advise FMPs to start preparing their documentation in accordance with the draft RTS on a best endeavours basis. Having supported numerous clients in preparing the entity and product level disclosures under the SFDR, we have observed first-hand that complying with this regulation represents a steep learning curve for most firms.

Preparing the disclosures now ensures firms are well placed to implement necessary changes in their ESG integration and data-gathering processes before the deadline hits.