The number of analysts predicting a sideways market in equities and bonds has risen, showing that uncertainty over geopolitics and the impact of US tariffs is still lingering

Political risk: Russia under pressure, maybe

Sometimes, political risk is positive. Donald Trump has given up on the Nobel Peace Prize, making Vladimir Putin the world’s major generator of political risk. The latest Russian budget acknowledges the glaring gap between income and expenditure. An increase in the VAT rate is considered, in spite of Putin’s promise not to increase taxes until 2030. Expenditure is dominated by the military. If that spending cannot be touched, cutting back on social spending is the only option. This would increase civil discontent.

Now that Germany, France and the UK have significantly increased their military budget, a second Putin pressure point is deliveries of NATO arms to Ukraine. The deliveries are notoriously slow, so Ukraine can still be lost, but if the arms come in time, they can neutralise the Russian strategy of massive attacks on land as well as by air. Since the US is unlikely to make much of an effort to participate in the Ukrainian theatre, it is now in practice no longer a player there.

Asset allocation: positive and neutral vote go head-to-head

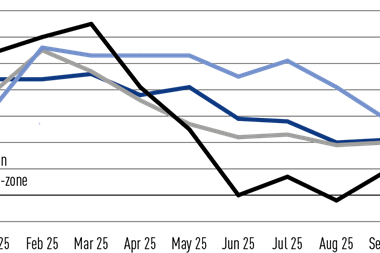

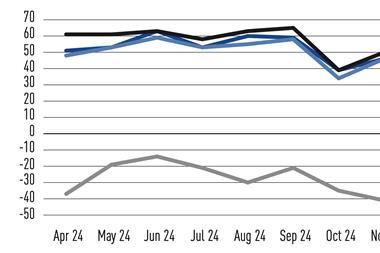

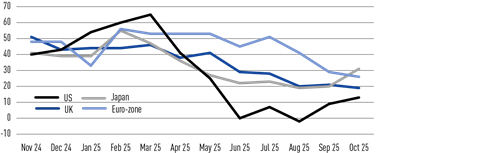

Net equity sentiment statistics are still converging to around +20 with the US recovering some ground from a low base, the EU and UK slowly climbing down and Japan going up to the point where it now, for the first time in the last 12 months, leads the pack. Since it is not clear what the optimism on Japanese equity is based on, there may be opportunities here.

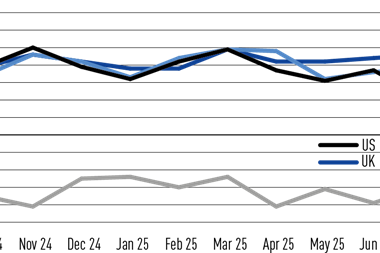

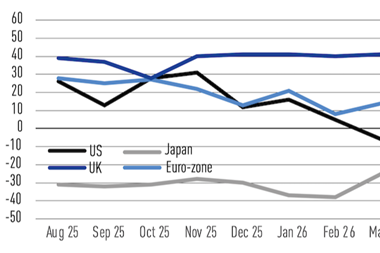

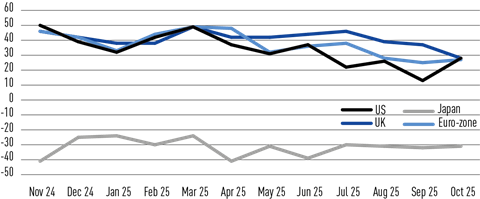

Net bond statistics are, again with the exception of Japan, converging quite precisely on a level of +30. Movements were very small and hard to interpret. In spite of Trump’s actions against the independence of the Fed and Powell suddenly looking like a moderate as Trump keeps appointing political allies, the US bond numbers climbed some.

The neutral vote remained at a very high level in all regions, signalling high uncertainty. With the exception of EU equity, all neutral scores increased or were flat and neutral equity and bond scores remained close together. This may be due to a feared influence of the Trump tariff wars on international trade.

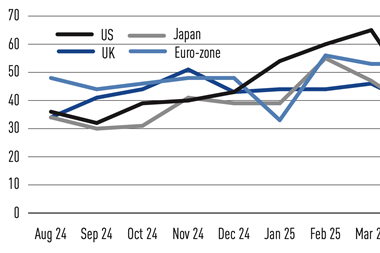

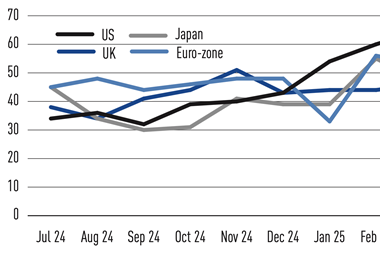

Country allocation: Japanese equities make comeback

US numbers are up, but still at a low level, with a preference for bonds that is now six months old. EU stats show a flat trend with an almost perfect convergence for equity and bonds. Japan analysts keep bonds at a sclerotic level of around -30, but equity is making a comeback. The UK graphs are converging, flat for equity and down for bonds, making the UK analysts slightly more pessimistic on equity than the EU analysts.

Net sentiment equities

Net sentiment bonds

Supporting documents

Click link to download and view these filesIPE Quest Expectations Indicator – October 2025

PDF, Size 0.53 mb