Finnish municipal pensions giant Keva announced this morning it will step up the risk level significantly in its investment portfolio, meaning in practice it will gradually boost its equities weighting.

In a statement, the €64bn occupational pension fund said: “Keva’s board has decided to increase the risk level of the investment portfolio. The change aims for a higher long-term return on investment assets.”

Explaining the background to the decision, Keva said that since 2017, when the pension provider’s pension costs began to exceed contributions, part of those costs had been financed with investment income.

In the future, investment income would become more important for pension funding, though pension contributions would remain the largest source of pension funding each year, the Helsinki-based pension fund said.

“From the point of view of the pension institution’s investment activities, the most important risk is the so-called long-term deficit risk, i.e. the risk that sufficient real returns are not achieved,” Keva said.

If that risk materialised, it said pension contributions would have to be increased.

“In the strategic planning of Keva’s investment activities, it has been observed that with the current risk level of the investment portfolio, it will be challenging to achieve a sufficient real return that secures a stable payment level in the future,” Keva noted.

“In response to this challenge, Keva’s board has decided that the risk level of investment operations will be increased significantly in the near future,” the institution said, adding that as the level of risk rose, expected long-term returns would increase.

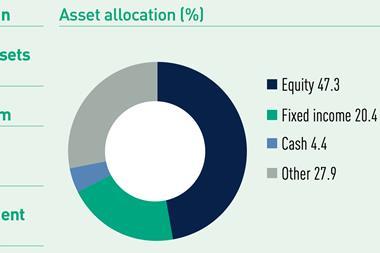

“The decision to increase the risk level means in practice that the share weight of the reference portfolio outlined by Keva’s board and which determines the overall risk level will be gradually increased,” Keva added.

“An increase in the risk level lowers the long-term deficit risk, but on the other hand, it means that the short-term return on investment assets fluctuates more than before,” the institution said.

Keva said that since 1988, it had produced a real return of a capital-weighted 3.6% or 4.8% on a non-capital-weighted basis. This meant, Keva said, that investment returns accounted for €46bn of its current €64bn of assets.

For Keva, it is the board of directors – currently chaired by Petteri Orpo, who became Finland’s prime minister in June – that determines the overall risk level for investment activities, and the fund’s investment department that then manages investment assets within the risk framework and scope for deviation.

While Keva’s board is able to change the fund’s risk level, on the private sector side of Finland’s earnings-related pension system, the pension insurance companies – such as Varma and Ilmarinen – are beholden to lawmakers to change their solvency level rules in order to make such changes to strategy.

There have been several calls from the private-sector providers for permission to increase investment risk levels recently.

In August, Ilmarinen’s president and chief executive officer Jouko Pölönen repeated his call for the solvency framework for earnings-related companies to be reshaped to enable them to seek better long-term returns.

Earlier this summer, Allan Paldanius, director of the Finnish Centre for Pensions, said private-sector occupational pension providers could lift returns by 0.3% on average by increasing equities weightings by 10 percentage points.

Read the digital edition of IPE’s latest magazine