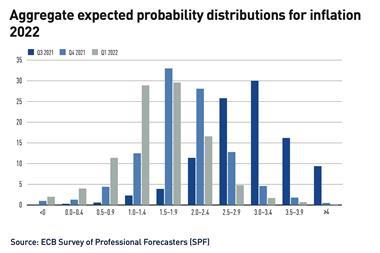

Investment chiefs at Nordic pension funds say they are expecting the European Central Bank (ECB) to tighten monetary policy, with its US and UK counterparts already having raised rates, after the outbreak of war in Ukraine put further upwards pressure on inflation.

In a blog posted on 13 March, Jesper Rangvid, professor of finance at Copenhagen Business School, said the Ukraine crisis had now contributed to increasing inflation even further, and argued that the ECB should tighten monetary policy.

Inflation had been very high for many months and the contribution to it from the “horrendous” situation in Ukraine left the central bank with a new dilemma, he said.

The consequences of the war threatened economic recovery in Europe, but if monetary policy was expansionary when inflation was already high, Rangvid said, inflation expectations rose, potentially causing developments similar to those of the 1970s.

“Even if there are dilemmas, I find that the ECB should tighten monetary policy,” he said.

Citing Rangvid’s view, IPE asked pension funds across the Nordic region for their opinions about the inflation situation now, after the Russian invasion of its neighbour at the end of February.

Magdalena Högberg, head of strategic allocation and quantitative analysis at AP4 in Sweden, said: “The Ukraine crisis has certainly increased the probability that inflation will stay elevated for longer and we will probably see lasting effects on, for instance, food and energy prices.”

While the Fed had already begun raising rates, she said the SEK528bn (€50.6bn) national pensions buffer fund believed that the situation faced by the ECB was different with a weaker recovery and high energy prices affecting the economy.

“While we believe that it is likely that the ECB might hike interest rates to zero, a further tightening remains unlikely this year,” she said.

The ECB announced on 11 March that it would decrease its bond-buying programmes over the next few months, though last Thursday, according to Reuters, ECB President Christine Lagarde told a conference in Frankfurt the bank would be in no hurry to raise interest rates.

The ECB’s key interest rates are currently between -0.5% and 0%.

In the UK, the Bank of England decided on Thursday to raise its bank rate to 0.75% from 0.5%.

In Denmark, Sampension CIO Henrik Olejasz Larsen noted inflation was on the rise, particularly in the US, but also to a lesser extent in Europe.

“The war in Ukraine will in the short-term add to supply frictions, especially in commodity markets, and thus to inflation,” he said.

The ECB may be cognisant of the uncertainty that can reduce consumption and investments in Europe, but the main scenario is that inflationary pressures will persist, and that demand will not weaken enough to hinder a more widespread inflation pressure,” he said.

“Thus we expect monetary policies to continue to tighten gradually for at least the coming year,” Olejasz Larsen told IPE.

Meanwhile in Finland, Kari Vatanen, CIO of pension insurance company Veritas, said inflation had surprised on the upside for several months now and Ukrainian war would even boost it higher than before.

But he said: “Core inflation figures have been quite moderate in Europe and it’s quite improbable that we will see huge wage inflation in this environment.”

Commodity inflation was hard to combat with monetary policy tools, Vatanen said.

“In fact, the monetary policy of the ECB has been very supportive for over a decade, but we haven’t seen inflation before this crisis,” he said.

“If easy monetary policy cannot create inflation, it is unclear if tight monetary policy can fight against this kind of commodity-driven inflation, based on the decreased supply,” the Veritas CIO said.

Commodity-driven inflation would only decrease when the supply and demand ratio changed, and that would take a long time for food and energy, he said.

“Maybe the ECB doesn’t have any other choice than to tighten monetary policy - it will hurt the economic growth first, and inflation will come down much later,” Vatanen said.

As for Veritas’ strategy, he said the pension provider had prepared for rising rates by decreasing the interest-rate sensitivity of our fixed income portfolio.

Potential problems could arise in equity and alternatives portfolios, he said, if rapidly-rising rates were to have a dramatic effect on the valuations of any risky assets.

“We are actively seeking potential places to be if rates, credit and equities suffer at the same time,” he said, adding that some factors and systematic strategies might help in that kind of environment.

In Norway, Harald Koch-Hagen, senior vice president risk management and allocation at KLP, said the Russian invasion of Ukraine had caused price shocks in energy prices, which could contribute to an accelerating price-wage spiral.

“With high inflation, falling unemployment and fairly healthy GDP growth in the eurozone, we would not be surprised if ECB signals a tighter monetary policy,” he said.

In the US and Norway, the central banks had already started raising rates, he observed.

Regarding KLP’s strategy, Koch-Hagen said: “We have not made changes in our overall investment strategy, but operationally our portfolio managers make tactical adjustments to adapt to the changing macro environment.”

“We find real assets to look attractive in these economic conditions, and continue to look for new opportunities,” he said.

Read the digital edition of IPE’s latest magazine