Investment in support of the UN’s Sustainable Development Goals (SDGs) has more than doubled over the last two years. Yet impact investing has aroused scepticism.

Impact Investing is a hot market. Long the domain of development finance institutions, impact investing has moved mainstream, with the likes of Bain Capital, Calvert, Goldman Sachs, JP Morgan, Merrill Lynch, Morgan Stanley, Temasek and Texas Pacific Group now offering impact fund alternatives.

Impact investing, an investment strategy that seeks to generate financial returns while creating a positive social or environmental impact, has grown 17% annually the past five years to $715bn assets under management involving 1,720 firms, according to a 2020 survey by the Global Impact Investing Network (GIIN).

Impact investing now accounts for 7% of all private investment assets under management, according to McKinsey.

Our analysis shows that entrepreneurs and investors are increasingly focused on environmental concerns. Investment in support of the UN’s Sustainable Development Goals (SDGs) has more than doubled over the last two years.

Yet impact investing has aroused skepticism. In “Is ‘impact investing’ just bad economics?,” Philip Demuth argues that impact investing muddles financial and charitable motives leaving investors wanting on both measures. Instead, he advised leaving investment to financial managers, while charities focus on donations.

Others worry about ‘impact washing,’ spurious investor claims of social impact without supporting evidence, a temptation that increases as governments impose ESG mandates. According to McKinsey, more than a quarter of assets under management operate according to ESG principles.

Economic merits of impacting investing

Dismissing impact investing altogether, as Demuth does, is bad economics. With sound judgment and rigour, impact investing may accomplish investment and charitable objectives more effectively jointly than when pursued separately.

Microeconomics is a balancing act. Production optimises where marginal cost and marginal productivity intersect. Manufacturers maximise production by balancing capital and labour. Consumers maximise utility by allocating discretionary spending across a basket of goods where price equals marginal utility. Similarly, impact investing optimises financial and social mandates by balancing these objectives across an asset portfolio.

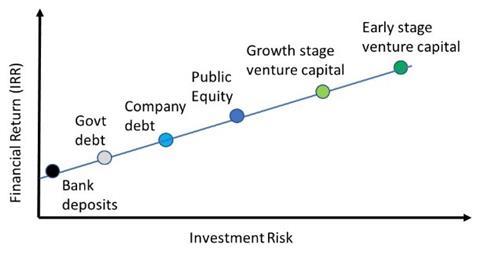

Financial economics describes an ‘efficient frontier’ as the optimal expected return for a given level of risk. As shown in figure 1, investors require a higher return on an illiquid, risky venture capital investment than a liquid, low risk government security or bank deposit.

Figure 1: Efficient frontier and market rates of return

The efficient frontier framework also applies to impact investing. A pure financial investment requires a risk-adjusted market rate of return independent of social impact. A grant requires high social impact to compensate for the opportunity cost of foregone financial return that might have been achieved by substituting an investment for a charitable donation.

Impact investing offer a middle path offering the prospect of both financial return and social impact. When economist William Baumol characterised innovation as productive, unproductive, and destructive, he acknowledged variance between economic impact and financial outcome. For example, novel technology, replicative innovation and criminal activity may product equal financial returns but have diametrically different economic impact. Financial and social objectives are thus not mutually exclusive.

Impact investing seeks to do good by doing well offering attractive financial returns while delivering positive societal impact. Financial returns and social impact are often mutually reinforcing. Venture capital has brought life changing innovations, economic growth, prosperity, and employment wherever it has flourished. No activity can do good if it does not do well: underperformance is unacceptable to donors and investors alike.

Impact investing involves real tradeoffs. Surveys indicate that 67% of impact investing assets under management are deployed for risk adjusted market rates of return. The other 33% accepts concessionary returns while seeking to return capital. As figure 2 shows, concessionary returns may be economically efficient if an investment provides sufficient additionality through social benefits that could not otherwise be achieved through financial objectives exclusively.

Figure 2: Efficient frontier for impact investing

eImpact investing advantages relative to grant funding

Grant funding addresses social needs in the non-profit sector where market friction obstructs for-profit initiatives. Sources of market friction are manifold. Public goods, externalities, knowledge spillovers, low-income markets with limited ability to pay, high transaction costs, frontier markets with political uncertainty, institutional constraints and regulatory uncertainty are just a few of the market frictions that many worthy non-profit organisations address.

Yet not all activities fit neatly into a bifurcated world of financial investment and social goods. Two by two matrices have intellectual appeal, yet such a bipolar world would be bleak. Impact investing thrives in the more nuanced world in which we live.

The economic principle of money velocity illustrates the advantages of impact investing. Money velocity measures the number of times currency is used to purchase goods and services during a given period. A supermarket with weekly inventory turns will have 26x higher money velocity than a car dealership with semi-annual inventory turns. Increased money velocity produces higher economic growth all else being equal.

Impact investing promises a return of capital while grant funding involves a single use of donor capital. Donor capital is gone once deployed, while impact investing, even when deployed at concessionary rates, uses capital multiple times. Capital may recycle five times with an 80% return of capital including administrative expenses and 10 times with a 90% return. A 100% return of capital may be redeployed indefinitely, and profitable returns offer a growing source of committed capital.

Fundraising for impact investing can be a tough sell despite its evident advantages over grant funding. Jacqueline Novogratz, founder of Acumen Fund, observed the challenges of pitching impact investment: “It never fails to amaze me how people seem comfortable making grants for purely charitable purposes, so they experience a 100% loss of their money and are equally comfortable investing in hopes of seeing financial returns of 10-20%, even if they risk losing a portion of principal. Yet these same individuals will often not consider investment that results in negative returns of 10-20% that creates outsized social impact. Between pure charity and pure financial return, there is an unexplored space with tremendous opportunities for innovation, social impact and lasting change.”

Demuth and Novogratz debate the essential question inherent in impact investing: should conscientious investors allocate financial and charitable capital from two pockets or one pocket. Two pocket investors separate financial investments and charitable contributions and commit capital along the X and Y axes in figure 2. Impact investing appeals to one pocket investors who seek financial and social returns along the continuum between A and C.

The growth of impact investing and entry of top tier firms suggest attractive financial returns and market demand for one pocket investing. As figure 3 shows, impact investors report 10-18% median equity returns and 7-10% debt returns across developed and emerging markets according to GIIN’s 2020 survey. Median concessionary discounts for below market versus market rate investors are 10-20% for lenders and 40-50% for equity investors.

Figure 3: Impact investor reported rates of return

Impact investing: additionality and demonstration effect

The growth of impact investing underscores an opportunity for socially responsible initiatives. Yet impact investing will add economic value only if there is additionality by investing in overlooked sectors beyond the reach of financial investors.

Impact investing must address gaps in the market. As noted earlier, market friction abounds. Investors systemically overlook frontier markets due to limited liquidity, political uncertainty, institutional constraints and exit options. As a result, 50% of the world population receives just 5% of global private investments and represents just 0.4% of global market capitalisation. Emerging markets lack neither talent nor opportunity, yet talented entrepreneurs often must go to the capital: over 25% of US venture funded companies are founded by immigrants.

Investments in public health, education, energy, agriculture, the environment and community enablement involve public goods with positive externalities that benefit many in society beyond the innovator. Over 40% of the world adult population are unbanked ignoring wealth at the bottom of the pyramid due to small transaction sizes and imperfect information. Without government support through patent protections and funding for basic research, the private sector systematically underinvests in research as scientific breakthroughs involve knowledge spillovers that no single entity cannot fully capture.

Acknowledging the importance of externalities, Nobel Prize winner Paul Krugman lamented: “The stuff that I stressed in the models is a less important story than the things I left out because I could not model them, like spillovers of information and social networks.”*

Impact investing at its best attracts mainstream capital into previously overlooked markets. The International Finance Corporation was an early investor in leading emerging market mobile operators such as Airtel in India, MTN in Africa and Orascom in the Middle East accelerating mobile adoption across emerging markets and attracting private investment. Microlenders Grameen Bank in Bangladesh, SKS Microfinance in India, BancoSol in Bolivia demonstrated profitable small lending to unbanked borrowers attracting bank competition and over $152bn of capital to an overlooked sector. MPesa in Africa, Alipay in China and PayTM in India have created robust mobile payment systems that have bolstered the digital economy in their respective markets and spurred emulation across other emerging markets.

Impact investing has risen to the top of the agenda for many of the world’s top investors and corporations. BlackRock, the world’s largest investor with $7trn under management has put sustainability at the top of its investment strategy. The World Business Council for Sustainable Development is a coalition of 120 international companies united by a shared commitment to the environment and to the principles of economic growth and sustainable development. Individual and corporate investors alike share a common consideration: where does your capital sleep at night. Impact investing is dedicated to the view that we sleep better when our capital is prudently seeking financial returns, while pursuing socially responsible objectives.

Impact investing has broadened the range of viable investments and unearthed overlooked opportunity. It has attracted private capital into sectors that were previously the exclusive province of donors and government funding. It may tap talent in underserved markets and unlock fortune at the bottom of the pyramid. The US share of global venture capital has declined from 83% in 2004 to below 50% in 2021. We believe this is a positive development, one that impact investing may perpetuate nurturing nascent ecosystems and enabling entrepreneurship to flourish elsewhere in the future.

*Larissa MacFarquhar, “The Deflationist: How Paul Krugman Found Politics,” New Yorker, 1 March 2010