MSCI is about to overhaul another of its climate benchmarks, in the latest sign of investor restlessness on the subject.

Following a consultation that closed in April, the MSCI Climate Action Indexes (CAI) Methodology is undergoing a number of major changes this month, including the adoption of a tilting approach, a simpler scoring system for how companies ‘manage’ climate, and more flexibility around the caps on issuer and sector exposures.

It will also be updated to incorporate more constituents with goals approved by the Science Based Targets initiative (SBTi), and have looser exclusions around nuclear weapons.

MSCI stated that most of the updates were being introduced “to reduce the ex-ante tracking error relative to the corresponding Parent Index”.

This concern about tracking error has been growing among investors as the global economy resists decarbonisation efforts, leading to unpalatable levels of divergence between climate indices and their parent benchmarks, and eating into risk budgets.

In January, IPE reported that Migros had given up on a Paris-aligned index it had licensed from MSCI in 2021, because the tracking error had grown too large.

The Swiss pension fund moved its foreign equity portfolio to a bespoke version of the CAI instead.

MSCI’s off-the-shelf CAI was designed in 2020, in partnership with Finnish private pension insurer Ilmarinen.

Juha Venäläinen, an equity strategist for Ilmarinen, told IPE that it was still using the index, and “welcomed” the latest efforts to reduce tracking error and turnover.

Bigger than one index

And the issue isn’t limited to investors using MSCI products.

According to data from Amundi, outflows from “higher-tracking-error strategies” in the sustainability space hit €10bn last year. Over the same period, there was some €26bn allocated to equivalents with lower tracking error.

The most ambitious climate benchmarks tend to reduce their exposure to carbon-intensive companies, explains Ross Finlayson, the head of markets and product strategy for Amundi’s ETF and indexing business.

“And those companies have generally performed well through recent energy shocks, which has created a challenging performance environment for ‘darker green’ strategies in the short term.”

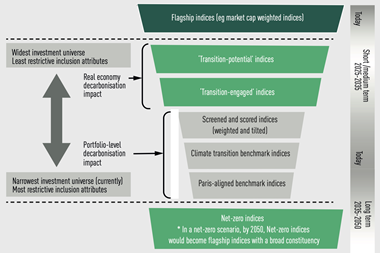

In 2024, Adrien Perret, the executive director of French pension fund Fonds de Réserve pour les Retraites (FRR) told IPE it “can’t use” off-the-shelf Paris Aligned (PAB) and Climate Transition Benchmarks, because the annual decarbonisation targets were likely to result in the exclusion of lots of companies.

He said at the time that this was “problematic from an investment perspective, but it also doesn’t achieve any real-world transition”. Now, the fund is designing its own index to overcome these challenges.

“The goal of FRR’s current work is to build more forward‑looking climate indices aimed at efficiently decarbonising the portfolio while taking the entire supply chain into account, maintaining exposure to all sectors, reflecting the strict fossil fuels exclusion policy and overweighting companies expected to play a critical role in the future transition,” Perret said in an update this week.

Swedish pension fund AP2, which was the first pension fund to make a significant allocation to an index with an EU PAB label, is also reconsidering its strategy.

Speaking to IPE last week, head of sustainability and communications Asa Norman said it was “still in the process of creating an updated approach” but had not yet concluded the process, and was therefore still using its PAB for the time being.

Achieving impact

New research from Scientific Portfolio highlights another challenge for pension funds grappling with climate indices.

The start-up, spun out from EDHEC Business School, assessed 18 ‘climate’ benchmarks and found that most exhibited a larger ‘overshoot’ in projected emissions than comparable market cap-weighted benchmarks.

The study also concluded that the indices were no more likely to invest in companies with credible emissions-reduction targets than their conventional counterparts.

“The next generation of climate-aligned indices should observe what’s happening in the economy as a whole”

Shahyar Safaee, Scientific Portfolio

“The majority were more aligned with climate risk considerations than net zero objectives,” explains Shahyar Safaee, the deputy chief executive officer of Scientific Portfolio.

He says this is a reasonable pursuit, but notes “how little focus on [net zero] alignment there is for most indices that are marketed as having a climate objective”.

To tackle both the tracking error dilemma and the lack of capital, many of these benchmarks channel towards decarbonisation, Safaee suggests a new approach.

“The next generation of climate-aligned indices should observe what’s happening in the economy as a whole, and in which sectors and regions, and use the real pace of decarbonisation to identify and invest in ambitious companies that lead the transition effort,” he argues.

“Rather than setting a decarbonisation target inferred from very long-term objectives and then trying to adhere to it.”