Troubled methodologies and unrealistic pathways have undermined the credibility of the process, but there are efforts to get it taken more seriously

Key points:

- Client Earth is urging the UK government to double down on climate scenario analysis

- The NGFS is rewriting its ‘damage function’ after problems with underlying research

- USS says a narrative approach is needed if it’s to be useful for investors

The UK government is under pressure to step up its expectations for how pension funds incorporate climate risks into their financial calculations.

ClientEarth wrote to secretary of state Steve Reed in March, urging him to consider the role of climate analysis in the upcoming valuation of Local Government Pension Schemes (LGPS).

“We’re asking the government to make clear that pension schemes must properly assess climate risks when carrying out their valuations,” explains Megan Clay, the legal campaign group’s head of European financial and economic systems.

“That means using credible climate scenario analysis, disclosing the results and ensuring investment decisions reflect the potential economic impacts of climate change.”

In turn, says Clay, trustees should ensure their advisers “provide robust climate scenario analysis and risk modelling that enables them to manage the risks climate change poses to investment returns”.

“The models being used are often worryingly deficient”

Megan Clay, head of European financial and economic systems at ClientEarth

Pension funds are already required under UK law to undertake scenario analysis, as part of duties to report in line with the Taskforce on Climate-related Financial Disclosures (TCFD).

But Clay believes “the models being used for such analysis are often worryingly deficient, predicting implausibly low financial impacts from climate change, even at warming levels that climate scientists consider catastrophic”.

Top-down difficulties

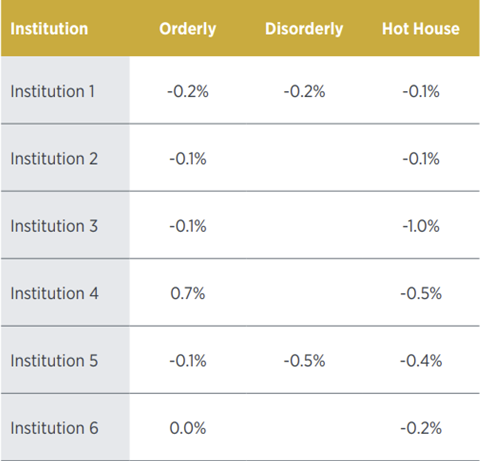

An anonymised sample of UK institutional investors, published by the Institute and Faculty of Actuaries in 2023 (see table), shows that – even under the most aggressive temperature trajectories – portfolio returns were estimated to see minimal impacts.

In 2024, research by academics at the Potsdam Institute for Climate Impact Research bucked the trend for conservative forecasts, estimating that unchecked climate change could slash global output by nearly 20% by 2050, and more than 60% by the end of the century.

The findings were quickly taken up by the World Bank, the OECD and the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) – the latter of which incorporated them into its influential ‘damage function’, used by financial institutions to help understand long-term economic impacts.

In a statement at the time, Sabine Mauderer, deputy government of the German Bundesbank and NGFS chair, said the updated scenario “mark[ed] an important step forward in our collective understanding of climate-related macroeconomic risks”.

“By incorporating the most recent climate commitments and enhanced risk modelling methodologies, we have significantly improved the accuracy of physical risk assessments,” she said, adding that “the new vintage assesses that GDP losses by 2050 could be two to four times greater than previously estimated”.

Widespread embarrassment soon followed when the paper was accused of producing exaggerated results, partly as a result of inaccurate underlying data.

The NGFS has pledged to re-design its damage function by the end of 2026.

For Jakob Thomae, co-founder and research director of climate think tank Theia Finance, the kind of top-down analysis being used for climate scenario analysis isn’t that helpful for investors, even when the underlying data is accurate.

“Do you really want to base your financial risk models on a global panel regression on the sensitivity of economic activity to temperature and precipitation changes, published in an academic paper? That’s way too macro to be a useful benchmark,” he tells IPE.

Instead, he thinks, investors should rely more on country-level climate data and analysis, produced by individual national governments.

Conviction missing

But Thomae claims the biggest hurdle for climate scenario analysis is that very few financial institutions take the pathways seriously.

“Most investors don’t actually believe in these climate scenarios, either because they’re unrealistically optimistic, in the case of 1.5°C, or – when it comes to the high emissions profiles – unrealistically pessimistic,” he argues.

“Which means it doesn’t matter how sophisticated you make the models: if you don’t have any conviction about the outcomes, they aren’t going to influence how you allocate capital.”

Instead, he says, the scenarios generally function either as a stress-testing exercise for perceived ‘extreme’ events, or to establish how aligned a portfolio is with implied temperature-rise metrics – the latter of which “is just another form of ESG score for a lot of investors”.

“2℃, 2.5℃ – these should be outputs from the analysis, not inputs”

Mirko Cardinale, head of investment strategy and advice at USS

Pension funds like the UK’s Universities Superannuation Scheme (USS) have decided to plough their own furrow.

“We very much agree with some of the criticism of traditional scenario analysis,” says Mirko Cardinale, the fund’s head of investment strategy and advice.

He says there’s a tendency to develop stand-alone climate pathways that don’t incorporate broader macroeconomic and market developments.

“You end up with scenarios that aren’t really decision useful, aren’t really plausible, and therefore aren’t integrated into the investment process,” Cardinale observes.

Narrative, not numbers

After undertaking traditional climate scenario analysis in 2022, USS decided to partner with academics at Exeter University the following year, to work out a new way to approach the process.

Cardinale says they were wary about the prevailing overemphasis on quantifying what is, in reality, a “very uncertain” future.

“We deliberately focused on the narrative instead,” he explains, avoiding anchoring scenarios to temperature pathways, as is common practice.

“2℃, 2.5℃ – these should be outputs from the analysis, not inputs,” he argues.

USS opted to look at the different ways the future might unfold in terms of policy, politics, technological innovations, and climate science.

It then identified plausible ranges for how key financial and economic metrics like GDP growth, inflation, equity returns and interest rates might be affected.

The research concluded that these areas could be negatively impacted by the likelihood of supply-side bottlenecks, geopolitical shocks and more pronounced boom and bust cycles in markets.

“So we stepped up our efforts to increase inflation protection across the portfolio and we strengthened our diversification in recognition of fundamental uncertainty on long-run macro and market outcomes,” explains Cardinale.

“We also reviewed our portfolio allocations to ensure that we can get through periods of volatility without being forced sellers, and are instead in a position to increase our exposure to attractive opportunities in those moments,” he adds.

USS replicated the process for other core macro drivers – including geopolitics and artificial intelligence – and brought all the findings together into a set of overarching scenarios, which it embeds into its investment decision-making.

“It’s not about optimising our asset allocations for the most likely outcome, because we don’t know what that is,” Cardinale notes.

“It’s about making the portfolio resilient enough to thrive under alternative futures.”