Despite the challenges posed by rising interest rates and the steep rise of the US dollar, none of the bigger emerging markets – such as Brazil, Mexico, Indonesia, Vietnam, South Africa and even Turkey – seem to be in debt distress, according to the latest analysis by the IMF, as well as looking at interest rate spreads.

In recent years, substantial economic activity and stubborn inflation led central banks to hike interest rates to levels not seen in decades. In 2023, these rising global rates, combined with a strong US dollar and tightening liquidity conditions, weighed on fixed income returns and wider market sentiment.

This proved particularly challenging for emerging markets debt (EMD). However, after a few years of lacklustre investment performance, we anticipate a strong 2024 for the asset class.

Normalising growth and policy easing

We believe in a significant improvement in the global macro backdrop in 2024, characterised by still-resilient economic growth, lower global rates, and improving global liquidity conditions.

While it appears likely that the global economy will continue to gradually decelerate, growth should remain close to its long-term potential. In that environment, central banks in advanced economies have likely reached the end of their hiking cycles, with monetary policy easing a predominant theme in 2024.

Many EM central banks have already started cutting policy rates, and we expect this process to continue into 2024, bearing in mind that in the global fight against inflation, EM central banks hiked interest rates sooner and faster than their counterparts in the developed world. As a result of such a timely and assertive policy reaction, inflation started to fall sooner and faster in EM countries.

In our opinion, easier monetary conditions will be one of the factors supporting economic growth in the EM world this year and beyond.

Stable credit fundamentals

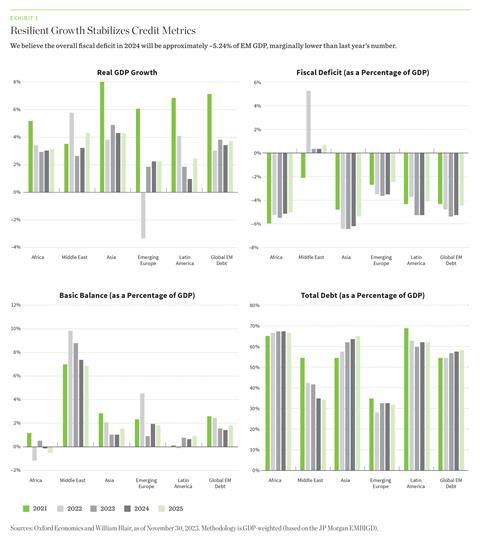

Additionally, credit fundamentals should remain well supported in most EM countries. We believe real gross domestic product (GDP) growth for our investment universe will be 3.5% in 2024, only marginally lower than in 2023.

We also expect stable fiscal and debt dynamics. We think the budget-balance deficit and total government debt should remain relatively stable at approximately 5.2% and 57.5% of GDP, respectively. From an external account perspective, we expect a basic balance (current account plus foreign direct investments) surplus of approximately 1.5% of GDP in 2024.

Technical conditions and valuations support EMD

In 2023, we saw substantial outflows from dedicated EMD portfolios as investors shied away from asset classes sensitive to interest rate duration risk. However, the market impact from sizable outflows was attenuated by muted activity in the primary market. Unfavourable financing conditions caused by rising interest rates led to another year of negative new net debt issuance, resulting in more balanced supply-and-demand dynamics in the marketplace.

EMD credit spreads appear compelling on both an absolute and relative basis, with current levels remaining wider than their historical levels. While EM sovereign high-grade credit spreads appear unattractive, high-yield credit spreads appear compelling, particularly relative to US corporate high yield levels. In the distressed credit space, we believe current prices continue to overestimate the probability of credit default and underestimate potential restructuring and recovery values.

For the local currency universe, headwinds of tighter US Federal Reserve policy and a stronger dollar have eased while interest rates in EMs remain elevated. Indeed, while several EM central banks have begun to loosen monetary policy, inflation has fallen faster than rates, leading to a widening of real interest rates.

With valuations in dollar terms little changed over the past year, the relative attractiveness of EM currencies against their developed market counterparts has risen substantially. We see further scope for modest currency appreciation over the coming year, led by high-beta countries.

Opportunities in EM corporate credit

We believe EM corporate credit is entering a period with normalising default expectations and diverse yet resilient fundamentals. The impact of higher-for-longer interest rates should become more apparent in the fundamental credit quality of EM corporate issuers in the next year.

However, despite some deterioration in leverage metrics in 2023, these metrics remain better than those of developed market credit and are likely to level off into next year. While coverage metrics should, in theory, deteriorate, it will likely depend on the composition of debt.

Weighing out the risks

While we have a high level of conviction in our constructive 2024 outlook, there are a few downside risks to our optimistic outlook.

We believe the Fed has reached the end of its hiking cycle and will start cutting policy rates at some point in the second half of 2024. However, keeping monetary policy conditions too tight for too long could result in a policy mistake that could lead to a US recession. Geopolitical tensions are also likely to continue to weigh on investor sentiment. The unresolved Russia/Ukraine conflict, instability in the Middle East, and tensions between China and Taiwan all have risks of escalation.

However, it is important to remember that there have always been potential incidents that could act as disruptors, and the current set of risks are already well known and perhaps fully priced by the markets already. We will nevertheless monitor all these risks very closely.

Marcelo Assalin is the head of emerging market debt at William Blair