The UK central bank has come out with a longer-term recommendation on how much liquidity defined benefit (DB) pension funds should be earmarking to service their liability-driven investment (LDI) funds in case of sudden rises in interest rates – as seen in September’s gilts market crisis.

The Bank of England (BoE), which already stated in December that as an interim measure DB pension funds needed to maintain 300-400 basis points of such financial resilience, said yesterday in a staff paper that on a steady-state basis, the pension funds should hold a minimum of 250 basis points of extra collateral for LDI funds.

However, other details in the paper, entitled “LDI minimum resilience – recommendation and explainer”, indicate a view from BoE officials that in total the buffers required may not be much lower than the interim recommendation made in December.

The advice from the Bank of England is mainly aimed at The Pensions Regulator (TPR), with the central bank having said back in December that regulators should set out appropriate ongoing minimum levels of resilience for LDI funds.

Outlining conclusions reached by the bank’s Financial Policy Committee (FPC) at a meeting earlier this month on what an appropriate steady-state minimum level of resilience for LDI funds should be, the bank said: “The FPC judged that these factors meant that the size of the yield shock to which LDI funds should be resilient should be, at a minimum, around 250 basis points […].”

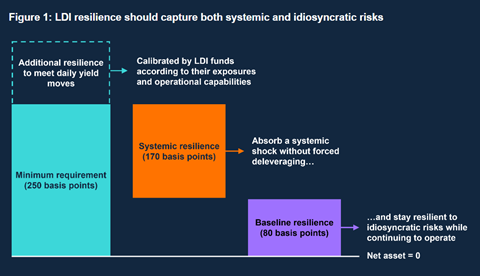

The minimum of 250 basis points has been conceived as the combination of 80 basis points minimum “baseline resilience” for LDI funds to stay resilient to idiosyncratic risks while continuing to operate, and at least 170 basis points for “systemic resilience”, designed to absorb a systemic shock without forced deleveraging, according to a graphic contained in the Bank of England’s staff paper released yesterday.

That graphic visually suggests that over and above the minimum 250 basis points of overall “resilience”, additional resilience to meet daily yield moves – to be calibrated by LDI funds according to their exposure and operational capabilities – might be around 100 basis points.

The bank said that until an appropriate framework incorporating the various elements of its recommendations was in place, the FPC judged that “TPR, in co-ordination with the FCA and other overseas regulators, should continue to ensure that LDI funds maintain the resilience that has been built up as set out in the FPC’s November 2022 recommendation”.

The Pensions and Lifetime Savings Association (PLSA) reacted to the FCP’s assessment, saying many of its members already held more buffer liquidity than the bank was advising they should have in a non-crisis situation.

Joe Dabrowski, deputy director of the industry association, said: “One of the most effective ways schemes can manage this [LDI] risk is by holding additional collateral, although this does come at the cost of potentially reducing some investment in growth assets.

“It is therefore important that recommended levels of collateral reflect the current stage of the interest rate cycle,” he said.

More than half of the DB funds surveyed by the PLSA were holding more than 250 basis points additional collateral in the wake of September’s mini-budget and had since strengthened their positions further given uncertainty about the future direction of monetary policy, Dabrowski said.

“The PLSA looks forward to seeing the regulator’s update of their stress testing, and underpinning analysis to see their assessment of systemic risks,” he said.

Meanwhile, consultancy LCP said it was unclear at this stage exactly how resilience was going to be monitored on an ongoing basis, with the Bank of England’s latest words on the topic being simple recommendations.

Zuhair Mohammed, head of LCP’s investment team, said the speed and severity of yield movements during the Gilt crises had shocked everyone.

“They were multiples larger than anything we’d seen in the previous 40 years. So it was no surprise that the TPR and joint regulators statement imposed a ‘temporary’ 300-400 basis point collateral requirement on LDI pooled funds,” he said.

Yesterday’s announcement by the Bank of England would not materially impact the way LDI mandates were run, he said.

“The devil’s going to be in the detail. These are recommendations at this stage, and we expect the TPR to respond with more detailed guidance,” said Mohammed.

To read the digital edition of IPE’s latest magazine click here