A range of new solutions and policy levers to attract greater pension fund investment in assets that have potential to drive growth in the UK economy have been identified by the Pensions and Lifetime Savings Association (PLSA).

The association detailed that today UK pension funds invest almost £1trn in the UK through a mixture of UK shares, corporate bonds, government debt, and other asset classes.

This investment generates the capital businesses need to expand their operations, hire more employees and develop new products and services. It also supports spending on infrastructure, renewable energy and social programmes.

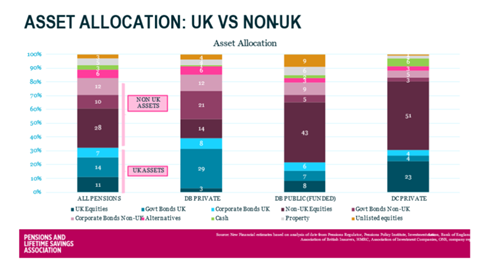

PLSA’s latest paper – Pensions & Growth – stated that pension funds are already large-scale owners of UK assets: about 32% of UK pension assets are invested in the UK, and around 50% overseas, with around 11% being invested in property and alternatives.

In the case of private sector defined benefit (DB) pension schemes, the allocation is 40% in the UK (equities and bonds), 47% in non-UK assets, and 10% in property and alternatives (some of which are in the UK).

In the case of open public sector DB funds, 21% invest in UK assets (equities and bonds), 57% in non-UK assets, and 9% in property and alternatives (some of which are UK).

Finally, for defined contribution (DC) pension schemes, 31% invest in UK assets (equities and bonds), 59% in non-UK assets, and 5% in property and alternatives (some of which are UK).

The association expects the scale and distribution of assets across the pensions sector to alter substantially over the next decade, during which time the volume of assets in DC pension schemes is expected to double to around £1trn and the value of assets in the Local Government Pension Scheme (LGPS) is forecast to increase up to around £500bn.

The value of private sector DB pension funds, PLSA said, is expected to remain at £1.5trn as most are closed to new members and future accrual, although as many as 500 schemes, managing assets of around £300bn, remain open.

Opportunities

The PLSA has identified several opportunities to encourage all types of pension funds to invest further in UK growth. Importantly, it said, these measures do not inhibit pension schemes’ ability to direct the investment of their members’ private savings, and do not dilute their fiduciary duty to scheme members.

This includes suitable UK investment opportunities, with the asset management industry expected to be focused on sourcing UK opportunities and developing new investment funds and products that are appropriate to pension fund needs.

The British Business Bank, the PLSA stated, should be given an extended scope to support companies that need scale up capital, and to create or partner with funds that can bundle up the assets in a form that would be suitable for pension funds.

Another opportunity listed by the association are fiscal incentives. It said that initiatives such as the Long-term Investment for Technology and Science, which alter the risk-return component of an investment, are appealing to pension funds provided the financial support from government is of a long-term nature.

It added that enhancing the tax treatment of domestic investments, as is done in France and Australia, merits exploration.

Lastly, the PLSA said that setting out a clear plan for the future of the UK economy, for example on the green transition, would help draw pension fund investment and allow the UK to compete with non-domestic assets.

Specific measures

The PLSA has also identified several measures, split between DC, DB and LGPS funds.

For DC pensions schemes, the associaiton said the market should be incentivised to ensure that those purchasing workplace pensions are focusing on ultimate member outcomes.

It added that the government should consider whether the Financial Conduct Authority (FCA) rules on suitability of “DC default funds” and the regime applying to corporate IFAs are fit for purpose.

It also highlighted the importance of the government pressing ahead with its plan to increase automatic enrolment contributions by removing the lower earnings limit and by starting auto-enrolment at age 18 instead of 22.

Measures specific to the LGPS include the Scheme Advisory Board’s Good Governance review, which the PLSA said should be implemented as soon as possible.

It added that following changes to the management of LGPS assets, which involved consolidating from around 90 separate pension funds into eight asset pools, the primary focus should now be on ensuring the current structures work well via the provision of guidance or regulation to support collaboration between and across funds and pools.

On DB funds measures, the PLSA said that more flexibility should be given to open DB pension funds than is currently planned in The Pensions Regulator’s DB Funding Code. It said that where supported by a strong employer covenant, open DB pension schemes should be able to carry long-term risks as part of their investment strategy, even as they approach maturity.

Nigel Peaple, director policy and advocacy at the PLSA, said: “How pension funds can play a bigger role in providing capital to support growth in the UK economy is an important question, and in our discussions with schemes there is a clear appetite to invest in the UK – where it is in the interests of savers.”

Read the digital edition of IPE’s latest magazine

Topics

- auto-enrolment

- Countries & Regions

- Defined benefit

- economic growth

- Financial Conduct Authority

- Financial Conduct Authority (FCA)

- funding code

- Local Government Pension Scheme (LGPS)

- Markets

- Pension System

- Pensions and Lifetime Savings Association (PLSA)

- Returns

- Solvency II

- The Pensions Regulator (TPR)

- United Kingdom