Railpen has created a framework to help investors assess their capacity to invest in illiquid assets and manage these investments through time.

The framework focuses on the illiquidity aspect of private markets, rather than the potential for additional return or diversification. It has been developed for Railpen’s 100+ defined benefit (DB) pension clients, including open and closed DB schemes.

Framework

The framework published today considers a number of elements to decide on the capacity for illiquidity, including client asset portfolio defining the opportunity set, expected returns and risk, and the strategic asset allocation of a client. It also considers client liquidity sources and uses, this includes pension benefit payments, asset class rebalancing, derivative position collateral needs, and private market cash flows.

More specifically for private markets, the framework incorporates asset class-specific cash flow profiles to capture unique liquidity characteristics that these investments exhibit.

It also considers portfolio liquidity risk management. It said that while the other three components generate client portfolio dynamics over time for a set of assumptions on asset portfolio, expected liquidity needs and private market cash flows, the framework defines relevant metrics against which client liquidity is measured, evaluated and managed.

Railpen said that the exact measures may differ by client; however, the general principle focuses on managing the medium-to-long-term risk of being forced to make unattractive and costly portfolio decisions to create needed liquidity.

With all these four building blocks in place, a simulated portfolio is run to generate a probabilistic assessment of portfolio liquidity and what-if analyses under different assumptions, Railpen said.

John Greaves, director of fiduciary management, said that allocation to illiquid assets is an important strategic consideration for Railpen that plays a significant role in achieving long-term client objectives.

He said: “We understand that an illiquid asset allocation that may be suitable for one portfolio, might not be fit-for-purpose for another due to different strategic client considerations.

“We have therefore developed this important framework to enable us to assess our different clients’ capacity for certain assets across the private markets spectrum from real estate to private equity.”

Case studies

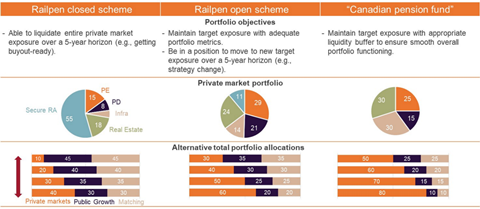

The research showcases the difference in capacity for illiquidity via three distinct illustrative clients: a Railpen closed scheme, a Railpen open scheme, and a hypothetical Canadian pension fund.

For a typical closed scheme aiming to fully liquidate the portfolio, Railpen said it is critical to have a sufficiently long runway to smoothly manage the exposure down, coupled with the ability/willingness to tap into the secondary market if needed.

For an open scheme, it is important to maintain high-quality private markets investment implementation, while also being in a position to steer the allocation to a new target in the case of a significant strategy change, Railpen said.

It added that while the “Canadian pension fund” is a less constrained investor, illiquidity capacity should also be considered for portfolios with high illiquid asset allocations. In particular, the research illustrates how liquidity buffers that are designed to withstand various portfolio liquidity events can help determine the appropriate level of illiquid asset exposure.

Greaves said: “There are a number of common threads running across all these illustrative client case studies.”

He said that taking into account client-unique objectives, constraints and opportunity sets should play a crucial role when evaluating capacity for illiquidity.

He added: “Any potential illiquid asset allocation should link up with these specific client requirements to deliver a portfolio that has the needed level of portfolio steerability.”

Greaves added that capturing all these considerations requires having the appropriate governance model through which client strategy is effectively linked to illiquid asset investment implementation.

Read the digital edition of IPE’s latest magazine