All articles by Peter Kraneveld – Page 2

-

Features

FeaturesIPE Quest Expectations Indicator - August 2024

Joe Biden’s weakness was a lucky stroke for Donald Trump, who has shown similar symptoms for years. It remains to be seen what effect Kamala Harris has on the polls. Trump and his chosen VP are both proponents of weakening the USD.

-

Features

FeaturesIPE Quest Expectations Indicator - June 2024

Trump and Biden are both losing to undecided voters, a group that is now unusually large and may be sensitive to Trump’s legal troubles. Biden’s approval rate is below his score in presidential polls, while Trump’s score is the same in presidential polls and those measuring voters’ opinion of him. In the UK, the Conservatives took another drubbing in the local elections.

-

Features

FeaturesIPE Quest Expectations Indicator - May 2024

EU parliamentary elections are approaching fast. Current polls predict a shift to the right, with the current centrist parties remaining dominant and the extremist right overtaking the Eurosceptics. US President Donald Trump is still liable to be convicted in a criminal case, but his poll figures are rising.

-

Features

FeaturesIPE Quest Expectations Indicator - April 2024

The shadow of the US presidential elections is longer than normal because Trump is under several legal clouds. He could still get barred from participating but that seems unlikely. He does have a liquidity problem, a self-destructive streak, a mercurial character and no credible alternative waiting in the wings, though.

-

Features

FeaturesIPE Quest Expectations Indicator - March 2024

Climate change is coming to a trend break as the low-hanging fruit has been picked.

-

Features

FeaturesIPE Quest Expectations Indicator - February 2024

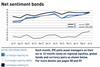

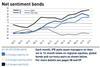

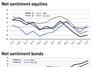

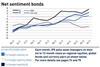

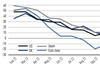

IPE’s monthly poll of market sentiment, asking 50 asset managers about their six to 12-month views on regional equities, global bonds and currency pairs

-

Features

FeaturesIPE Quest Expectations Indicator - January 2024

It is safe to predict that 2024 will be a year of desperate campaigning. Political surprises in the US and UK are possible and, this time, they do make a difference to markets

-

Features

FeaturesIPE Quest Expectations Indicator - December 2023

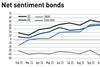

IPE’s monthly poll of market sentiment, asking 50 asset managers about their six to 12-month views on regional equities, global bonds and currency pairs

-

Features

FeaturesIPE Quest Expectations Indicator - November 2023

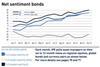

IPE’s monthly poll of market sentiment, asking 50 asset managers about their six to 12-month views on regional equities, global bonds and currency pairs

-

Features

FeaturesIPE Quest Expectations Indicator - October 2023

The Russian war in the Ukraine is still stalling, with the prelude of the US elections coming closer. Trump’s self-destructive utterings keep his followers unmoved but do nothing to convince independents.

-

Features

FeaturesIPE Quest Expectations Indicator: September 2023

US officials are talking up the Ukrainian advance towards Melitopol, a sign that all is not well. Contrary to expectations, the biggest problem is not the Russian air force, but land mines. Trump’s legal problems are as worrisome as his inexplicable lead among Republicans. US abstinence in the struggle against climate change is a potential cause for a major trade war as the EU realises it must expand its regulations on importing ‘dirty’ products to prevent a free rider problem undermining its climate efforts. In the UK, Labour’s lead over the Conservatives remains crushing, making it difficult to claim the government has a popular mandate.

-

Features

FeaturesIPE Quest Expectations Indicator: July 2023

The war in Ukraine is starting to look like a stalemate. This would be in Russia’s favour. Delivery to Ukraine of more of the tanks promised or fighters to contest Russian air control might lead to a breakthrough, but is unlikely to happen in the summer. In the US, Trump looks like a leading but weak candidate for the Republicans, even against a Democrat as unpopular as Biden. Legal pushbacks against the fight to prevent permanent climate change, notably in Texas, have the potential to cause a trade war with the EU. They illustrate how European and North American values are slowly drifting apart.

-

Features

FeaturesIPE Quest Expectations Indicator: August 2023

Politics is on hold until September. Normally, markets do not care and analysts reduce their activity. A political crisis in the Netherlands shows the danger. There are warnings from all sides that climate measures are ever more urgently needed. Markets need a clearer view of which products govern- ments will support with market-shaping measures and when, especially in the face of a faltering pace towards climate goals. Early signs of problems include a lack of capital for innovative start-ups and the increasingly loud voices of climate change deniers.

-

Features

FeaturesIPE Quest Expectations Indicator: June 2023

Continued loud bickering between the Wagner Group and the Russian army is protecting Putin from both, worsening the outlook for peace, while there are multiple signs that military supplies are approaching exhaustion. The coalition supporting Ukraine is stronger than ever, showing increasing willingness to provide military aircraft. Yet the offensive expected in February has not started. In the US, Florida governor Ron DeSantis is damaging his position with an unproductive row with Disney, while Trump has moved closer to a prison term. Gas consumption in the EU is falling faster than expected, due to efficiencies like heat pumps, changeover to electricity and solar panels. Macron scored nicely by sponsoring the participation of Zelensky at the Hiroshima G7; Sunak failed to centre political attention on China.

-

Features

FeaturesIPE Quest Expectations Indicator May 2023

Russian air superiority over Ukraine is coming to an end due to lack of equipment. Destroying civilian targets is counterproductive and consumes ammunition. Bakhmut is eating into Russian resources, while Ukraine is being re-armed. History teaches that better technology, rather than numerical superiority, wins wars. But even a lopsided Ukrainian win would not automatically mean peace.

-

Features

FeaturesIPE Quest Expectations Indicator April 2023

With new, superior equipment, the Ukrainian military is set to start an offensive soon. Meanwhile, Yevgeny Prigozhin, leader of the Wagner Group, is jockeying to become Russia’s next kleptocrat on the back of the Russian army. Donald Trump’s candidacy is increasingly beleaguered by defeats in court. The trade agreement on Northern Ireland between the EU and the UK is a significant boon for both as well as for Prime Minister Rishi Sunak, not because the trade flows are so important but because the issue blocked co-operation in many other fields. While the winter has been mild and beneficial, there are early signs of a dry spring, quite possible in view of climate change setting in. If that materialises, harvests, therefore food prices, will be affected in autumn.

-

Opinion Pieces

Opinion PiecesViewpoint: The power of prioritisation

When you can’t decide on return and risk, you think of the window of light

-

Features

FeaturesIPE Quest Expectations Indicator March 2023

The next Ukrainian offensive will be in April at the earliest, as modern tanks will have arrived by then. US Republican pushback of ESG and climate-related investments are a new bone of contention in relations with the EU, already strained by the Trump presidency, and a bad sign for US-EU co-operation on China policy, an issue Japan seems to be ducking successfully. Aided by a soft winter, EU energy concerns have become quite manageable.

-

Features

FeaturesIPE Quest Expectations Indicator: February 2023

Russian attacks against Ukrainian civilians are hampered by efficient air defence. With weapons for the Ukrainian military on the way, a new offensive seems imminent. US President Joe Biden’s troubles over classified documents are a relief for Republicans. The threat of a US-EU trade conflict over China is growing as both sides retreat into nationalistic behaviour. In the UK, Conservatives are under threat of predicted historic losses, while Prime Minister Rishi Sunak so far has done nothing to repair relations with the EU.

-

Features

FeaturesIPE Quest Expectations Indicator - January 2023

Better air defence and the ground freezing over are steadily improving the outlook for Ukraine’s forces, now locked in stalemate. A series of blunders haunts US Republicans in general and Trump in particular. If Biden’s stimulus package is enacted, it will counteract Fed policy, possibly prolonging the series of interest rate increases. The EU seems to have bought too much gas. It has agreed to take border measures against some products from climate change laggard countries.