Data published by the UK’s Office for National Statistics (ONS) this week has revealed that the introduction of auto-enrolment in 2012 has led to the proportion of workers saving in a workplace pension increasing by more than half.

From 6 April this year, minimum contributions for employers into auto-enrolment plans rose to 3% from 2% of salary, while employees must now pay 5%, up from 3%.

In 2012, when the first major UK companies were compelled to enrol full-time employees into a pension scheme, the ONS said 49.8% of the UK private sector workforce had some form of occupational pension savings. By the end of last year, this proportion had risen to 76.2%, according to the statistics bureau.

In 1997, at the start of the ONS’ data series, 55.2% of workers in the private sector had some form of pension savings. The majority were members of a defined benefit (DB) scheme (45.7%), while defined contribution (DC) plans accounted for just 8.7%.

By 2012, DB coverage had fallen to 29.4% of the workforce, but DC was still just 8.4%. In the intervening period, use of group stakeholder and group personal pensions – alternative versions of traditional DC plans – grew their market share to collectively account for 11.6% of private sector workers.

Since the introduction of auto-enrolment, DB membership as a proportion of the private sector workforce has fallen gradually to 27.8%. In contrast, regular DC plans now account for 25.9%, and group personal and group stakeholder arrangements have 20.9%.

Chris Connelly, propositions and solutions director at administration provider Equiniti, highlighted that “perhaps the most transformational element” of auto-enrolment was the increase in coverage for younger workers. People aged at least 22 and earning at least £10,000 (€11,560) are eligible for auto-enrolment.

“Once again it was the youngest who saw the biggest rise in participation with a six percentage point increase in scheme membership for 22-29 year olds – in total, 79% now have a workplace pension,” Connelly said.

“Obviously with minimum contributions starting to rise, hopefully people are now starting to see the long-term value in a pension pot and will not opt out. With great new innovations like the pensions dashboard looming into view, it is heartening that the industry is not standing by and admiring the success of auto-enrolment, but putting a framework in place that will help people value what they have and seek to save more.”

Further reading

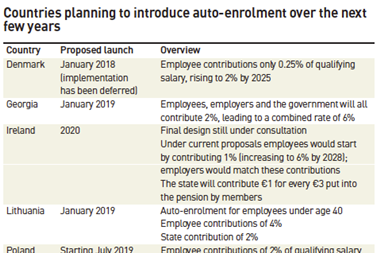

Auto-enrolment grows globally

A growing number of countries are planning to reduce the strain placed on public finances of providing pensions to ever more retirees by encouraging individuals to make more adequate provision for their own retirement

Auto-enrolment: A call for clarity

The UK government should set out its long-term policy on auto-enrolment contributions with a view to increasing the overall level, argues Jenny Condron, chair of the Association of Consulting Actuaries